Note

Click here to download the full example code

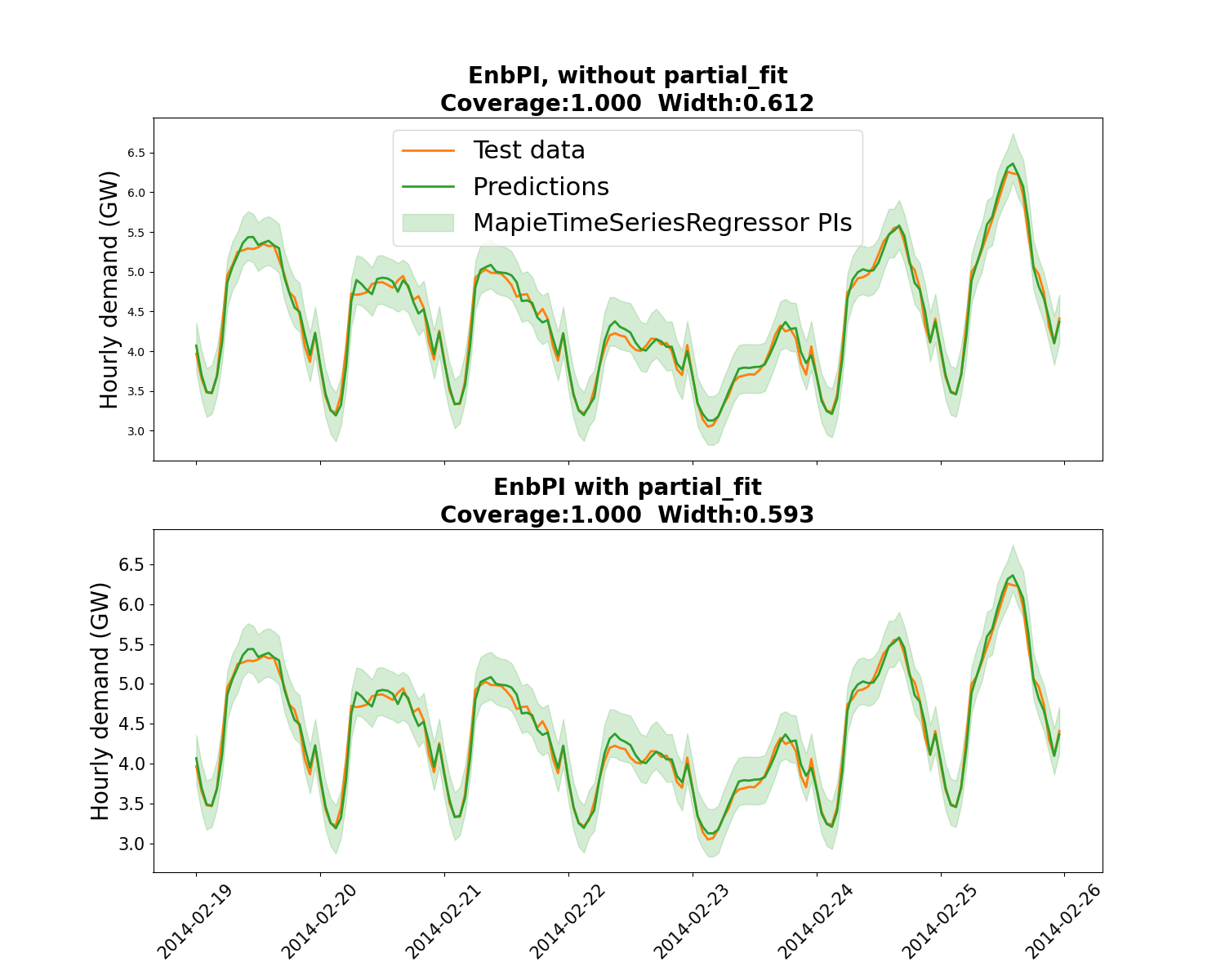

Estimating prediction intervals of time series forecast with EnbPI¶

This example uses

MapieTimeSeriesRegressor to estimate

prediction intervals associated with time series forecast. It follows [6].

We use here the Victoria electricity demand dataset used in the book “Forecasting: Principles and Practice” by R. J. Hyndman and G. Athanasopoulos. The electricity demand features daily and weekly seasonalities and is impacted by the temperature, considered here as a exogeneous variable.

A Random Forest model is already fitted on data. The hyper-parameters are

optimized with a RandomizedSearchCV using a

sequential TimeSeriesSplit cross validation,

in which the training set is prior to the validation set.

The best model is then feeded into

MapieTimeSeriesRegressor to estimate the

associated prediction intervals. We compare two approaches: with or without

partial_fit called at every step following [6]. It appears that

partial_fit offer a coverage closer to the targeted coverage, and with

narrower PIs.

Out:

EnbPI, with no partial_fit, width optimization

EnbPI with partial_fit, width optimization

Coverage / prediction interval width mean for MapieTimeSeriesRegressor:

EnbPI without any partial_fit:1.000, 0.612

Coverage / prediction interval width mean for MapieTimeSeriesRegressor:

EnbPI with partial_fit:1.000, 0.593

import warnings

from typing import cast

import numpy as np

import pandas as pd

from matplotlib import pylab as plt

from scipy.stats import randint

from sklearn.ensemble import RandomForestRegressor

from sklearn.model_selection import RandomizedSearchCV, TimeSeriesSplit

from mapie._typing import NDArray

from mapie.metrics import (regression_coverage_score,

regression_mean_width_score)

from mapie.regression import MapieTimeSeriesRegressor

from mapie.subsample import BlockBootstrap

warnings.simplefilter("ignore")

# Load input data and feature engineering

url_file = (

"https://raw.githubusercontent.com/scikit-learn-contrib/MAPIE/"

+ "master/examples/data/demand_temperature.csv"

)

demand_df = pd.read_csv(url_file, parse_dates=True, index_col=0)

demand_df["Date"] = pd.to_datetime(demand_df.index)

demand_df["Weekofyear"] = demand_df.Date.dt.isocalendar().week.astype("int64")

demand_df["Weekday"] = demand_df.Date.dt.isocalendar().day.astype("int64")

demand_df["Hour"] = demand_df.index.hour

n_lags = 5

for hour in range(1, n_lags):

demand_df[f"Lag_{hour}"] = demand_df["Demand"].shift(hour)

# Train/validation/test split

num_test_steps = 24 * 7

demand_train = demand_df.iloc[:-num_test_steps, :].copy()

demand_test = demand_df.iloc[-num_test_steps:, :].copy()

features = ["Weekofyear", "Weekday", "Hour", "Temperature"] + [

f"Lag_{hour}" for hour in range(1, n_lags)

]

X_train = demand_train.loc[

~np.any(demand_train[features].isnull(), axis=1), features

]

y_train = demand_train.loc[X_train.index, "Demand"]

X_test = demand_test.loc[:, features]

y_test = demand_test["Demand"]

perform_hyperparameters_search = False

if perform_hyperparameters_search:

# CV parameter search

n_iter = 100

n_splits = 5

tscv = TimeSeriesSplit(n_splits=n_splits)

random_state = 59

rf_model = RandomForestRegressor(random_state=random_state)

rf_params = {"max_depth": randint(2, 30), "n_estimators": randint(10, 100)}

cv_obj = RandomizedSearchCV(

rf_model,

param_distributions=rf_params,

n_iter=n_iter,

cv=tscv,

scoring="neg_root_mean_squared_error",

random_state=random_state,

verbose=0,

n_jobs=-1,

)

cv_obj.fit(X_train, y_train)

model = cv_obj.best_estimator_

else:

# Model: Random Forest previously optimized with a cross-validation

model = RandomForestRegressor(

max_depth=10, n_estimators=50, random_state=59

)

# Estimate prediction intervals on test set with best estimator

alpha = 0.05

cv_mapietimeseries = BlockBootstrap(

n_resamplings=10, n_blocks=10, overlapping=False, random_state=59

)

mapie_enpbi = MapieTimeSeriesRegressor(

model,

method="enbpi",

cv=cv_mapietimeseries,

agg_function="mean",

n_jobs=-1,

)

print("EnbPI, with no partial_fit, width optimization")

mapie_enpbi = mapie_enpbi.fit(X_train, y_train)

y_pred_npfit_enbpi, y_pis_npfit_enbpi = mapie_enpbi.predict(

X_test, alpha=alpha, ensemble=True, optimize_beta=True

)

coverage_npfit_enbpi = regression_coverage_score(

y_test, y_pis_npfit_enbpi[:, 0, 0], y_pis_npfit_enbpi[:, 1, 0]

)

width_npfit_enbpi = regression_mean_width_score(

y_pis_npfit_enbpi[:, 1, 0], y_pis_npfit_enbpi[:, 0, 0]

)

print("EnbPI with partial_fit, width optimization")

mapie_enpbi = mapie_enpbi.fit(X_train, y_train)

y_pred_pfit_enbpi = np.zeros(y_pred_npfit_enbpi.shape)

y_pis_pfit_enbpi = np.zeros(y_pis_npfit_enbpi.shape)

step_size = 1

(

y_pred_pfit_enbpi[:step_size],

y_pis_pfit_enbpi[:step_size, :, :],

) = mapie_enpbi.predict(

X_test.iloc[:step_size, :], alpha=alpha, ensemble=True, optimize_beta=True

)

for step in range(step_size, len(X_test), step_size):

mapie_enpbi.partial_fit(

X_test.iloc[(step - step_size):step, :],

y_test.iloc[(step - step_size):step],

)

(

y_pred_pfit_enbpi[step:step + step_size],

y_pis_pfit_enbpi[step:step + step_size, :, :],

) = mapie_enpbi.predict(

X_test.iloc[step:(step + step_size), :],

alpha=alpha,

ensemble=True,

optimize_beta=True,

)

coverage_pfit_enbpi = regression_coverage_score(

y_test, y_pis_pfit_enbpi[:, 0, 0], y_pis_pfit_enbpi[:, 1, 0]

)

width_pfit_enbpi = regression_mean_width_score(

y_pis_pfit_enbpi[:, 1, 0], y_pis_pfit_enbpi[:, 0, 0]

)

# Print results

print(

"Coverage / prediction interval width mean for MapieTimeSeriesRegressor: "

"\nEnbPI without any partial_fit:"

f"{coverage_npfit_enbpi :.3f}, {width_npfit_enbpi:.3f}"

)

print(

"Coverage / prediction interval width mean for MapieTimeSeriesRegressor: "

"\nEnbPI with partial_fit:"

f"{coverage_pfit_enbpi:.3f}, {width_pfit_enbpi:.3f}"

)

enbpi_no_pfit = {

"y_pred": y_pred_npfit_enbpi,

"y_pis": y_pis_npfit_enbpi,

"coverage": coverage_npfit_enbpi,

"width": width_npfit_enbpi,

}

enbpi_pfit = {

"y_pred": y_pred_pfit_enbpi,

"y_pis": y_pis_pfit_enbpi,

"coverage": coverage_pfit_enbpi,

"width": width_pfit_enbpi,

}

results = [enbpi_no_pfit, enbpi_pfit]

# Plot estimated prediction intervals on test set

fig, axs = plt.subplots(

nrows=2, ncols=1, figsize=(15, 12), sharex="col"

)

for i, (ax, w, result) in enumerate(

zip(axs, ["EnbPI, without partial_fit", "EnbPI with partial_fit"], results)

):

ax.set_ylabel("Hourly demand (GW)", fontsize=20)

ax.plot(demand_test.Demand, lw=2, label="Test data", c="C1")

ax.plot(

demand_test.index,

result["y_pred"],

lw=2,

c="C2",

label="Predictions",

)

y_pis = cast(NDArray, result["y_pis"])

ax.fill_between(

demand_test.index,

y_pis[:, 0, 0],

y_pis[:, 1, 0],

color="C2",

alpha=0.2,

label="MapieTimeSeriesRegressor PIs",

)

ax.set_title(

w + "\n"

f"Coverage:{result['coverage']:.3f} Width:{result['width']:.3f}",

fontweight="bold",

size=20

)

plt.xticks(size=15, rotation=45)

plt.yticks(size=15)

axs[0].legend(prop={'size': 22})

plt.show()

Total running time of the script: ( 0 minutes 23.854 seconds)