Note

Go to the end to download the full example code.

Adaptive conformal predictions for time series, Zaffran et al. (2022)

Note: in this example, we use the following terms employed in the scientific literature:

alpha is equivalent to 1 - confidence_level. It can be seen as a risk level

calibrate and calibration are equivalent to conformalize and conformalization.

—

TimeSeriesRegressor is used to reproduce a part of the paper experiments of Zaffran et al. (2022) in their article [1] which we argue that Adaptive Conformal Inference (ACI, Gibbs & Candès, 2021) [2], developed for distribution-shift time series, is a good procedure for time series with general dependency.

For a given model, the simulation adjusts the MAPIE regressors using aci method, on a dataset taken from the article and available on the github repository https://github.com/mzaffran/AdaptiveConformalPredictionsTimeSeries and compares the bounds of the PIs.

In order to reproduce the results of the github repository, we reuse the RandomForestRegressor regression model and follow the same conformal prediction procedure (see in AdaptiveConformalPredictionsTimeSeries project the models.py file).

This simulation is carried out to check that the aci method implemented in MAPIE gives the same results as [1], and that the bounds of the PIs are obtained.

[1] Zaffran, M., Féron, O., Goude, Y., Josse, J., & Dieuleveut, A. (2022). Adaptive conformal predictions for time series. In International Conference on Machine Learning (pp. 25834-25866). PMLR.

[2] Gibbs, I., & Candes, E. (2021). Adaptive conformal inference under distribution shift. Advances in Neural Information Processing Systems, 34, 1660-1672.

# sphinx_gallery_thumbnail_number = 2

import datetime

import pickle

import ssl

import warnings

from urllib.request import urlopen

import numpy as np

import pandas as pd

from matplotlib import pylab as plt

from sklearn.ensemble import RandomForestRegressor

from sklearn.model_selection import PredefinedSplit

from mapie.conformity_scores import AbsoluteConformityScore

from mapie.regression import TimeSeriesRegressor

warnings.simplefilter("ignore")

Global random forests parameters

def init_model():

# the number of trees in the forest

n_estimators = 1000

# the minimum number of samples required to be at a leaf node

# (default skgarden's parameter)

min_samples_leaf = 1

# the number of features to consider when looking for the best split

# (default skgarden's parameter)

max_features = 6

model = RandomForestRegressor(

n_estimators=n_estimators,

min_samples_leaf=min_samples_leaf,

max_features=max_features,

random_state=1,

)

return model

Get data

def get_data() -> pd.DataFrame:

"""

Get the data from a CSV file containing prices from 2016 to 2019.

Returns

-------

pd.DataFrame

The DataFrame containing the price data.

"""

# Backup committed in the MAPIE repository (see examples/data/README.md), so

# this example does not depend on the authors' repository. If the backup is

# unavailable, the original source is used instead.

backup = (

"https://raw.githubusercontent.com/scikit-learn-contrib/MAPIE/master/"

"examples/data/zaffran2022_prices.csv.gz"

)

original = (

"https://raw.githubusercontent.com/"

"mzaffran/AdaptiveConformalPredictionsTimeSeries/"

"131656fe4c25251bad745f52db3c2d7cb1c24bbb/data_prices/"

"Prices_2016_2019_extract.csv"

)

ssl._create_default_https_context = ssl._create_unverified_context

try:

return pd.read_csv(backup)

except Exception:

return pd.read_csv(original)

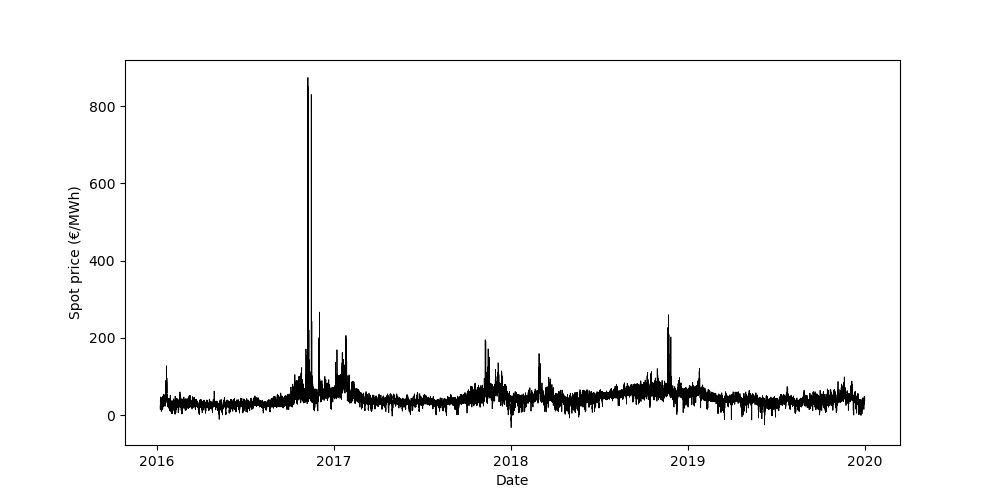

Get & Present data

data = get_data()

date_data = pd.to_datetime(data.Date)

plt.figure(figsize=(10, 5))

plt.plot(date_data, data.Spot, color="black", linewidth=0.6)

locs, labels = plt.xticks()

new_labels = ["2016", "2017", "2018", "2019", "2020"]

plt.xticks(locs[0 : len(locs) : 2], labels=new_labels)

plt.xlabel("Date")

plt.ylabel("Spot price (\u20ac/MWh)")

plt.show()

Prepare data

limit = datetime.datetime(2019, 1, 1, tzinfo=datetime.timezone.utc)

id_train = data.index[pd.to_datetime(data["Date"], utc=True) < limit].tolist()

data_train = data.iloc[id_train, :]

sub_data_train = data_train.loc[

:,

["hour", "dow_0", "dow_1", "dow_2", "dow_3", "dow_4", "dow_5", "dow_6"]

+ ["lag_24_%d" % i for i in range(24)]

+ ["lag_168_%d" % i for i in range(24)]

+ ["conso"],

]

all_x_train = [

np.array(sub_data_train.loc[sub_data_train.hour == h]) for h in range(24)

]

sub_data = data.loc[

:,

["hour", "dow_0", "dow_1", "dow_2", "dow_3", "dow_4", "dow_5", "dow_6"]

+ ["lag_24_%d" % i for i in range(24)]

+ ["lag_168_%d" % i for i in range(24)]

+ ["conso"],

]

all_x = [np.array(sub_data.loc[sub_data.hour == h]) for h in range(24)]

all_y = [np.array(data.loc[data.hour == h, "Spot"]) for h in range(24)]

Select Data (hour 0)

Prepare model

iteration_max = 10

alpha = 0.1

gamma = 0.04

model = init_model()

mapie_aci = TimeSeriesRegressor(

model,

method="aci",

agg_function="mean",

conformity_score=AbsoluteConformityScore(sym=True),

cv=PredefinedSplit(test_fold=[-1] * n_half + [0] * n_half),

random_state=1,

)

Reproduce experiment and results

y_pred_aci_pfit = np.zeros(((365,)))

y_pis_aci_pfit = np.zeros(((365, 2, 1)))

for i in range(min(test_size, iteration_max + 1)):

x_train = np.array(X[i : (train_size + i),])

x_test = np.array(X[(train_size + i),]).reshape(1, -1)

y_train = np.array(Y[i : (train_size + i)])

y_test = np.array(Y[(train_size + i)]).reshape(1, -1)

# Fit the model with new tran/calib dataset

mapie_aci = mapie_aci.fit(x_train, y_train)

# Predict on test dataset

y_pred_aci_pfit[i : i + 1], y_pis_aci_pfit[i : i + 1] = mapie_aci.predict(

x_test, confidence_level=1 - alpha, ensemble=False, optimize_beta=False

)

# Update the current_alpha_t (hidden for the user)

mapie_aci.adapt_conformal_inference(

x_test, y_test, gamma=gamma, ensemble=False, optimize_beta=False

)

results = y_pis_aci_pfit.copy()

Get referenced result to reproduce

def get_reference_results() -> dict:

"""

Get the reference results to reproduce.

Returns

-------

dict

A dict containing the reference lower (``Y_inf``) and upper (``Y_sup``)

prediction interval bounds.

"""

# Backup committed in the MAPIE repository (see examples/data/README.md), so

# this example does not depend on the authors' repository. If the backup is

# unavailable, the original pickle is used instead.

backup = (

"https://raw.githubusercontent.com/scikit-learn-contrib/MAPIE/master/"

"examples/data/zaffran2022_aci_reference.csv"

)

original = (

"https://github.com/mzaffran/AdaptiveConformalPredictionsTimeSeries/raw/"

"131656fe4c25251bad745f52db3c2d7cb1c24bbb/results/"

"Spot_France_Hour_0_train_2019-01-01/ACP_0.04_RF.pkl"

)

ssl._create_default_https_context = ssl._create_unverified_context

try:

df = pd.read_csv(backup)

return {

"Y_inf": df["Y_inf"].to_numpy().reshape(1, -1),

"Y_sup": df["Y_sup"].to_numpy().reshape(1, -1),

}

except Exception:

return pickle.load(urlopen(original))

data_ref = get_reference_results()

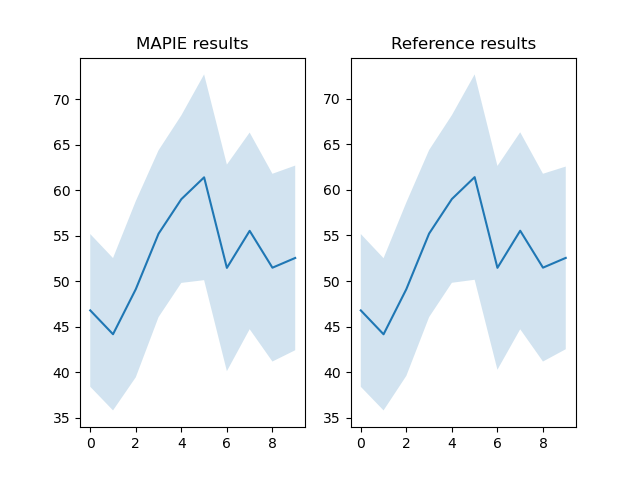

Compare results

# Flatten the array to shape (n, 2)

results_ref = np.concatenate([data_ref["Y_inf"], data_ref["Y_sup"]], axis=0).T

results = np.array(results.reshape(-1, 2))

# Compare the NumPy array with the corresponding DataFrame columns

comparison_result_Y_inf = np.allclose(

results[:iteration_max, 0], results_ref[:iteration_max, 0], rtol=1e-2

)

comparison_result_Y_sup = np.allclose(

results[:iteration_max, 1], results_ref[:iteration_max, 1], rtol=1e-2

)

comparison_result_Y_pred = np.allclose(

y_pred_aci_pfit[:iteration_max],

np.sum(results_ref, -1)[:iteration_max] / 2,

rtol=1e-2,

)

# Print the comparison results

# The results are very closed but not exactly the same because of the quantile

# calculation. In MAPIE, we use method="higher" when in the code of Zaffran,

# it use method="midpoint".

final_results = pd.DataFrame(

{

"y_inf": results[:iteration_max, 0],

"y_inf (ref)": results_ref[:iteration_max, 0],

"y_sup": results[:iteration_max, 1],

"y_sup (ref)": results_ref[:iteration_max, 1],

"y_pred": y_pred_aci_pfit[:iteration_max],

"y_pred (ref)": np.sum(results_ref, -1)[:iteration_max] / 2,

}

).round(2)

idx = np.arange(iteration_max)

fig, axs = plt.subplots(1, 2)

axs[0].fill_between(idx, final_results["y_inf"], final_results["y_sup"], alpha=0.2)

axs[0].plot(final_results["y_pred"])

axs[0].set_title("MAPIE results")

axs[1].fill_between(

idx, final_results["y_inf (ref)"], final_results["y_sup (ref)"], alpha=0.2

)

axs[1].plot(final_results["y_pred (ref)"])

axs[1].set_title("Reference results")

plt.show()

print(final_results)

print(f"Comparison for ACP_0.04 (Y_inf): {comparison_result_Y_inf}")

print(f"Comparison for ACP_0.04 (Y_sup): {comparison_result_Y_sup}")

print(f"Comparison for ACP_0.04 (Y_pred): {comparison_result_Y_pred}")

y_inf y_inf (ref) y_sup y_sup (ref) y_pred y_pred (ref)

0 38.33 38.40 55.20 55.16 46.76 46.78

1 35.77 35.81 52.54 52.51 44.16 44.16

2 39.39 39.60 58.78 58.62 49.09 49.11

3 45.96 46.04 64.43 64.37 55.19 55.21

4 49.74 49.81 68.20 68.20 58.97 59.00

5 50.12 50.14 72.78 72.67 61.45 61.40

6 39.92 40.27 62.93 62.63 51.43 51.45

7 44.62 44.71 66.41 66.32 55.51 55.52

8 40.86 41.17 62.09 61.77 51.48 51.47

9 42.19 42.52 62.80 62.56 52.50 52.54

Comparison for ACP_0.04 (Y_inf): True

Comparison for ACP_0.04 (Y_sup): True

Comparison for ACP_0.04 (Y_pred): True

Total running time of the script: (2 minutes 27.021 seconds)