Note

Go to the end to download the full example code.

Data with gamma distribution

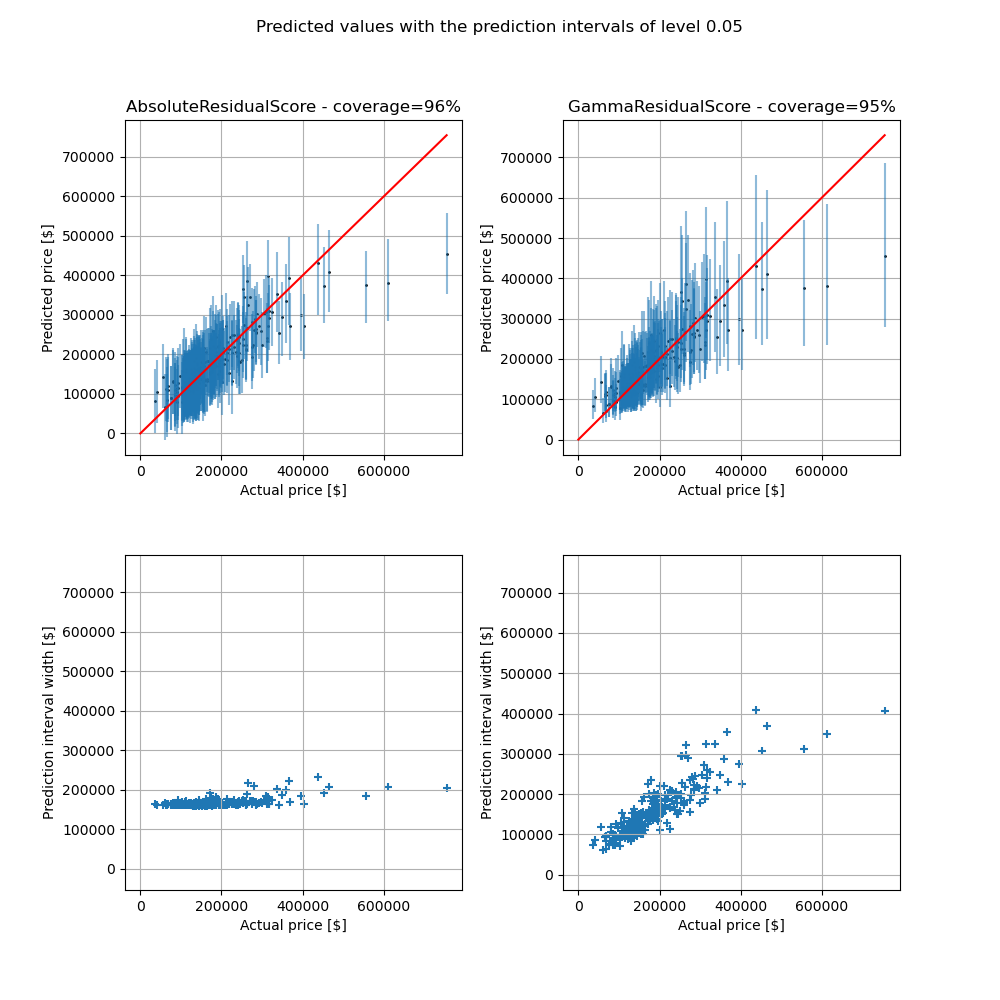

This example uses CrossConformalRegressor to estimate prediction intervals associated with Gamma distributed target. The limit of the absolute residual conformity score is illustrated.

We use here the OpenML house_prices dataset: https://www.openml.org/search?type=data&sort=runs&id=42165&status=active.

Note : OpenML is down as of 14/01/25, so we’ll load the data from Kaggle instead.

The data is modelled by a Random Forest model RandomForestRegressor with a fixed parameter set. The prediction intervals are determined by means of the MAPIE regressor CrossConformalRegressor considering two conformity scores: “absolute” which considers the absolute residuals as the conformity scores and “gamma” which considers the residuals divided by the predicted means as conformity scores. We consider the standard CV+ resampling method.

We would like to emphasize one main limitation with this example. With the default conformity score, the prediction intervals are approximately equal over the range of house prices which may be inapporpriate when the price range is wide. The Gamma conformity score overcomes this issue by considering prediction intervals with width proportional to the predicted mean. For low prices, the Gamma prediction intervals are narrower than the default ones, conversely to high prices for which the confidence intervals are higher but visually more relevant. The empirical coverage is similar between the two conformity scores.

import io

import zipfile

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import requests

from sklearn.ensemble import RandomForestRegressor

from sklearn.model_selection import train_test_split

from mapie.metrics.regression import regression_coverage_score

from mapie.regression import CrossConformalRegressor

RANDOM_STATE = 42

# Parameters

features = [

"MS SubClass",

"Lot Area",

"Overall Qual",

"Overall Cond",

"Garage Area",

]

target = "SalePrice"

confidence_level = 0.95

rf_kwargs = {"n_estimators": 10, "random_state": RANDOM_STATE}

model = RandomForestRegressor(**rf_kwargs)

1. Load dataset with a target following approximativeley a Gamma distribution

We start by loading a dataset with a target following approximately a Gamma distribution. Two sub datasets are extracted: the training and test ones.

dataset_url = (

"https://www.kaggle.com"

+ "/api/v1/datasets/download/shashanknecrothapa/ames-housing-dataset"

)

r = requests.get(dataset_url, stream=True)

with zipfile.ZipFile(io.BytesIO(r.content)) as z:

with z.open("AmesHousing.csv") as file:

data = pd.read_csv(file)

X = data[features]

y = data[target]

X_train_conformalize, X_test, y_train_conformalize, y_test = train_test_split(

X[features], y, test_size=0.2, random_state=RANDOM_STATE

)

2. Train model with two conformity scores

Two models are trained with two different conformity score:

conformity_score = “absolute” (default conformity score) is relevant for target positive as well as negative. The prediction interval widths are, in this case, approximately the same over the range of prediction.

conformity_score = “gamma” is relevant for target following roughly a Gamma distribution. The prediction interval widths scale with the predicted value.

First, train model with conformity_score = “absolute”.

mapie = CrossConformalRegressor(

model, confidence_level=confidence_level, conformity_score="absolute"

)

mapie.fit_conformalize(X_train_conformalize, y_train_conformalize)

y_pred_absconfscore, y_pis_absconfscore = mapie.predict_interval(X_test)

coverage_absconfscore = regression_coverage_score(y_test, y_pis_absconfscore)[0]

Prepare the results for matplotlib. Get the prediction intervals and their corresponding widths.

def get_yerr(y_pred, y_pis):

return np.concatenate(

[

np.expand_dims(y_pred, 0) - y_pis[:, 0, 0].T,

y_pis[:, 1, 0].T - np.expand_dims(y_pred, 0),

],

axis=0,

)

yerr_absconfscore = get_yerr(y_pred_absconfscore, y_pis_absconfscore)

pred_int_width_absconfscore = y_pis_absconfscore[:, 1, 0] - y_pis_absconfscore[:, 0, 0]

Then, train the model with: conformity_score = “gamma”.

mapie = CrossConformalRegressor(

model, confidence_level=confidence_level, conformity_score="gamma"

)

mapie.fit_conformalize(X_train_conformalize, y_train_conformalize)

y_pred_gammaconfscore, y_pis_gammaconfscore = mapie.predict_interval(X_test)

coverage_gammaconfscore = regression_coverage_score(y_test, y_pis_gammaconfscore)[0]

yerr_gammaconfscore = get_yerr(y_pred_gammaconfscore, y_pis_gammaconfscore)

pred_int_width_gammaconfscore = (

y_pis_gammaconfscore[:, 1, 0] - y_pis_gammaconfscore[:, 0, 0]

)

3. Compare the prediction intervals

Once the models have been trained, we now compare the prediction intervals obtained from the two conformity scores. We can see that the “absolute” `conformity score generates prediction interval with almost the same width for all the predicted values. Conversely, the `”gamma” conformity score yields prediction interval with width scaling with the predicted values.

The choice of the conformity score depends on the problem we face.

fig, axs = plt.subplots(2, 2, figsize=(10, 10))

for img_id, y_pred, y_err, cov, class_name, int_width in zip(

[0, 1],

[y_pred_absconfscore, y_pred_gammaconfscore],

[yerr_absconfscore, yerr_gammaconfscore],

[coverage_absconfscore, coverage_gammaconfscore],

["AbsoluteResidualScore", "GammaResidualScore"],

[pred_int_width_absconfscore, pred_int_width_gammaconfscore],

):

axs[0, img_id].errorbar(

y_test,

y_pred,

yerr=y_err,

alpha=0.5,

linestyle="None",

)

axs[0, img_id].scatter(y_test, y_pred, s=1, color="black")

axs[0, img_id].plot(

[0, max(max(y_test), max(y_pred))],

[0, max(max(y_test), max(y_pred))],

"-r",

)

axs[0, img_id].set_xlabel("Actual price [$]")

axs[0, img_id].set_ylabel("Predicted price [$]")

axs[0, img_id].grid()

axs[0, img_id].set_title(f"{class_name} - coverage={cov:.0%}")

xmin, xmax = axs[0, img_id].get_xlim()

ymin, ymax = axs[0, img_id].get_ylim()

axs[1, img_id].scatter(y_test, int_width, marker="+")

axs[1, img_id].set_xlabel("Actual price [$]")

axs[1, img_id].set_ylabel("Prediction interval width [$]")

axs[1, img_id].grid()

axs[1, img_id].set_xlim([xmin, xmax])

axs[1, img_id].set_ylim([ymin, ymax])

fig.suptitle(

f"Predicted values with the prediction intervals of level {confidence_level}"

)

plt.subplots_adjust(wspace=0.3, hspace=0.3)

plt.show()

Total running time of the script: (0 minutes 7.319 seconds)