Note

Click here to download the full example code

Tutorial for residual normalised score¶

We will use the sklearn california housing dataset to understand how the residual normalised score works and show the multiple ways of using it.

We will explicit the experimental setup below.

import warnings

import matplotlib.pyplot as plt

import numpy as np

from matplotlib.ticker import FormatStrFormatter

from numpy.typing import ArrayLike

from sklearn.datasets import fetch_california_housing

from sklearn.ensemble import RandomForestRegressor

from sklearn.linear_model import LinearRegression

from sklearn.model_selection import train_test_split

from mapie.conformity_scores import ResidualNormalisedScore

from mapie.metrics import regression_coverage_score_v2, regression_ssc_score

from mapie.regression import MapieRegressor

warnings.filterwarnings("ignore")

random_state = 23

rng = np.random.default_rng(random_state)

round_to = 3

1. Data¶

The target variable of this dataset is the median house value for the California districts. This dataset is composed of 8 features, including variables such as the age of the house, the median income of the neighborhood, the average number of rooms or bedrooms or even the location in latitude and longitude. In total there are around 20k observations.

data = fetch_california_housing()

X = data.data

y = data.target

Now let’s visualize a histogram of the price of the houses.

fig, axs = plt.subplots(1, 1, figsize=(5, 5))

axs.hist(y, bins=50)

axs.set_xlabel("Median price of houses")

axs.set_title("Histogram of house prices")

axs.xaxis.set_major_formatter(FormatStrFormatter('%.0f' + "k"))

plt.show()

Let’s now create the different splits for the dataset, with a training,

calibration, residual and test set. Recall that the calibration set is used

for calibrating the prediction intervals and the residual set is used to fit

the residual estimator used by the

ResidualNormalisedScore.

np.array(X)

np.array(y)

X_train, X_test, y_train, y_test = train_test_split(

X,

y,

random_state=random_state,

test_size=0.02

)

X_train, X_calib, y_train, y_calib = train_test_split(

X_train,

y_train,

random_state=random_state

)

X_calib_prefit, X_res, y_calib_prefit, y_res = train_test_split(

X_calib,

y_calib,

random_state=random_state,

test_size=0.5

)

2. Models¶

We will now define 4 different ways of using the residual normalised score.

Remember that this score is only available in the split setup. First, the

simplest one with all the default parameters :

a LinearRegression is used for the residual

estimator. (Note that to avoid negative values it is trained with the log

of the features and the exponential of the predictions are used).

It is also possible to use it with cv="prefit" i.e. with

the base model trained beforehand. The third setup that we illustrate here

is with the residual model prefitted : we can set the estimator in parameters

of the class, not forgetting to specify prefit="True". Finally, as an

example of the exotic parameterisation we can do : we use as a residual

estimator a LinearRegression wrapped to avoid

negative values like it is done by default in the class.

class PosEstim(LinearRegression):

def __init__(self):

super().__init__()

def fit(self, X, y):

super().fit(

X, np.log(np.maximum(y, np.full(y.shape, np.float64(1e-8))))

)

return self

def predict(self, X):

y_pred = super().predict(X)

return np.exp(y_pred)

base_model = RandomForestRegressor(n_estimators=10, random_state=random_state)

base_model = base_model.fit(X_train, y_train)

residual_estimator = RandomForestRegressor(

n_estimators=20,

max_leaf_nodes=70,

min_samples_leaf=7,

random_state=random_state

)

residual_estimator = residual_estimator.fit(

X_res, np.abs(np.subtract(y_res, base_model.predict(X_res)))

)

wrapped_residual_estimator = PosEstim().fit(

X_res, np.abs(np.subtract(y_res, base_model.predict(X_res)))

)

# Estimating prediction intervals

STRATEGIES = {

"Default": {

"cv": "split",

"conformity_score": ResidualNormalisedScore()

},

"Base model prefit": {

"cv": "prefit",

"estimator": base_model,

"conformity_score": ResidualNormalisedScore(

split_size=0.5, random_state=random_state

)

},

"Base and residual model prefit": {

"cv": "prefit",

"estimator": base_model,

"conformity_score": ResidualNormalisedScore(

residual_estimator=residual_estimator,

random_state=random_state,

prefit=True

)

},

"Wrapped residual model": {

"cv": "prefit",

"estimator": base_model,

"conformity_score": ResidualNormalisedScore(

residual_estimator=wrapped_residual_estimator,

random_state=random_state,

prefit=True

)

},

}

y_pred, intervals, coverage, cond_coverage = {}, {}, {}, {}

num_bins = 10

alpha = 0.1

for strategy, params in STRATEGIES.items():

mapie = MapieRegressor(**params, random_state=random_state)

if mapie.conformity_score.prefit:

mapie.fit(X_calib_prefit, y_calib_prefit)

else:

mapie.fit(X_calib, y_calib)

y_pred[strategy], intervals[strategy] = mapie.predict(X_test, alpha=alpha)

coverage[strategy] = regression_coverage_score_v2(

y_test, intervals[strategy]

)

cond_coverage[strategy] = regression_ssc_score(

y_test, intervals[strategy], num_bins=num_bins

)

def yerr(y_pred, intervals) -> ArrayLike:

"""

Returns the error bars with the point prediction and its interval

Parameters

----------

y_pred: ArrayLike

Point predictions.

intervals: ArrayLike

Predictions intervals.

Returns

-------

ArrayLike

Error bars.

"""

return np.abs(np.concatenate(

[

np.expand_dims(y_pred, 0) - intervals[:, 0, 0].T,

intervals[:, 1, 0].T - np.expand_dims(y_pred, 0),

],

axis=0,

))

def plot_predictions(y, y_pred, intervals, coverage, cond_coverage, ax=None):

"""

Plots y_true against y_pred with the associated interval.

Parameters

----------

y: ArrayLike

Observed targets

y_pred: ArrayLike

Predictions

intervals: ArrayLike

Prediction intervals

coverage: float

Global coverage

cond_coverage: float

Maximum violation coverage

ax: matplotlib axes

An ax can be provided to include this plot in a subplot

"""

if ax is None:

fig, ax = plt.subplots(figsize=(6, 5))

ax.set_xlim([-0.5, 5.5])

ax.set_ylim([-0.5, 5.5])

error = y_pred - intervals[:, 0, 0]

warning1 = y_test > y_pred + error

warning2 = y_test < y_pred - error

warnings = warning1 + warning2

ax.errorbar(

y[~warnings],

y_pred[~warnings],

yerr=np.abs(error[~warnings]),

color="g",

alpha=0.2,

linestyle="None",

label="Inside prediction interval"

)

ax.errorbar(

y[warnings],

y_pred[warnings],

yerr=np.abs(error[warnings]),

color="r",

alpha=0.3,

linestyle="None",

label="Outside prediction interval"

)

ax.scatter(y, y_pred, s=3, color="black")

ax.plot([0, max(max(y), max(y_pred))], [0, max(max(y), max(y_pred))], "-r")

ax.set_title(

f"{strategy} - coverage={coverage:.0%} " +

f"- max violation={cond_coverage:.0%}"

)

ax.set_xlabel("y true")

ax.set_ylabel("y pred")

ax.legend()

ax.grid()

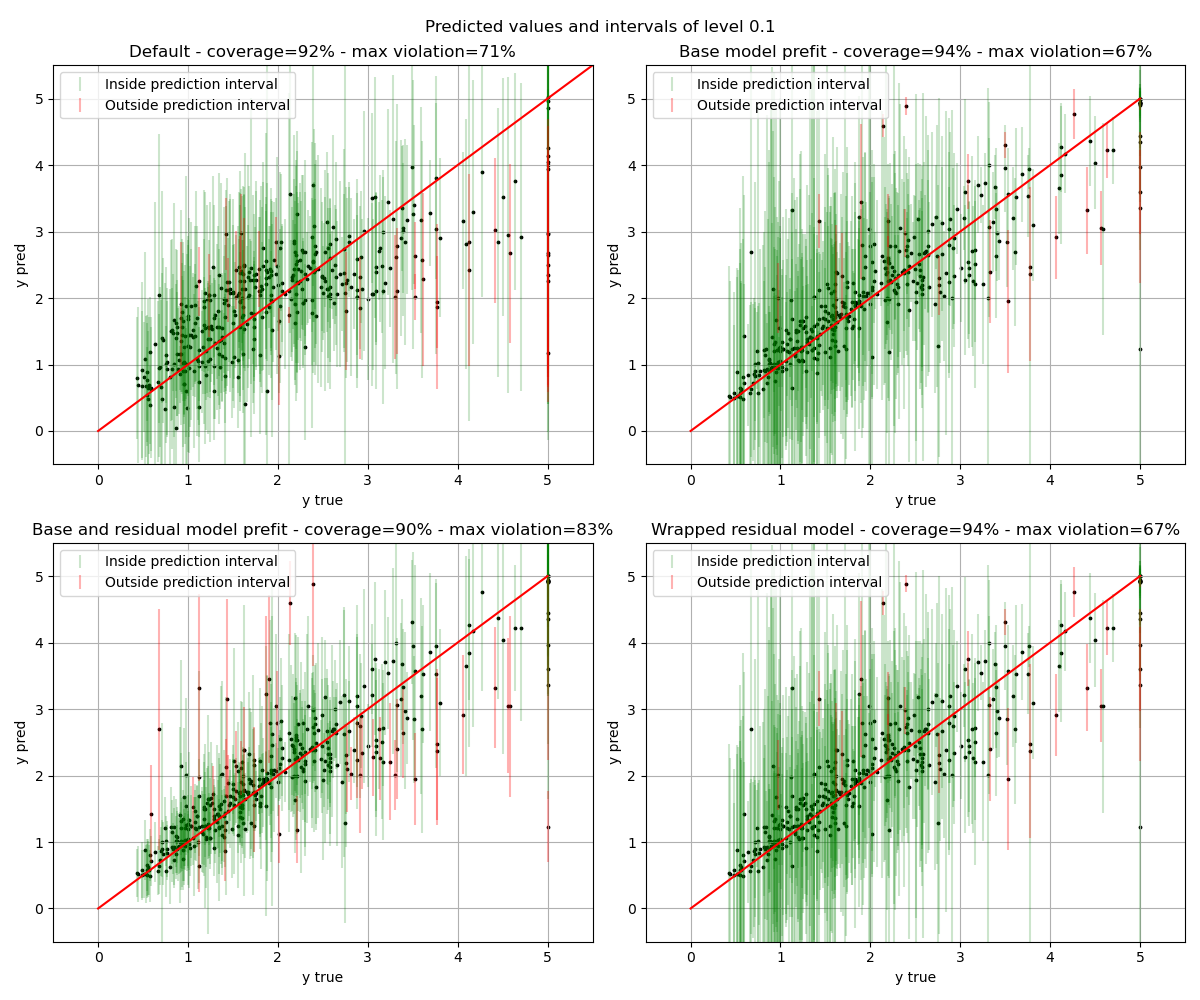

fig, axs = plt.subplots(nrows=2, ncols=2, figsize=(12, 10))

for ax, strategy in zip(axs.flat, STRATEGIES.keys()):

plot_predictions(

y_test,

y_pred[strategy],

intervals[strategy],

coverage[strategy][0],

cond_coverage[strategy][0],

ax=ax

)

fig.suptitle(f"Predicted values and intervals of level {alpha}")

plt.tight_layout()

plt.show()

The results show that all the setups reach the global coverage guaranteed of 1-alpha. It is interesting to note that the “base model prefit” and the “wrapped residual model” give exactly the same results. And this is because they are the same models : one prefitted and one fitted directly in the class.

Total running time of the script: ( 0 minutes 3.626 seconds)