Note

Go to the end to download the full example code.

Conformalized quantile regression on gamma distributed data

We will use the sklearn california housing dataset as the base for the comparison of the different methods available on MAPIE. Two classes will be used: ConformalizedQuantileRegressor for CQR. We use CrossConformalRegressor and JackknifeAfterBootstrapRegressor for the other methods.

For this example, the estimator will be LGBMRegressor with objective=”quantile” as this is a necessary component for CQR, the regression needs to be from a quantile regressor.

We then compare the coverage and the intervals width.

# sphinx_gallery_thumbnail_number = 3

import warnings

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

from lightgbm import LGBMRegressor

from matplotlib.offsetbox import AnnotationBbox, TextArea

from matplotlib.ticker import FormatStrFormatter

from scipy.stats import randint, uniform

from sklearn.datasets import fetch_california_housing

from sklearn.model_selection import KFold, RandomizedSearchCV, train_test_split

from mapie.metrics.regression import (

regression_coverage_score,

regression_mean_width_score,

)

from mapie.regression import (

ConformalizedQuantileRegressor,

CrossConformalRegressor,

JackknifeAfterBootstrapRegressor,

)

RANDOM_STATE = 1

rng = np.random.default_rng(RANDOM_STATE)

round_to = 3

warnings.filterwarnings("ignore")

1. Data

The target variable of this dataset is the median house value for the California districts. This dataset is composed of 8 features, including variables such as the age of the house, the median income of the neighborhood, the average number rooms or bedrooms or even the location in latitude and longitude. In total there are around 20k observations. As the value is expressed in thousands of $ we will multiply it by 100 for better visualization (note that this will not affect the results).

data = fetch_california_housing(as_frame=True)

X = pd.DataFrame(data=data.data, columns=data.feature_names)

y = pd.DataFrame(data=data.target) * 100

Let’s visualize the dataset by showing the correlations between the independent variables.

df = pd.concat([X, y], axis=1)

pear_corr = df.corr(method="pearson")

pear_corr.style.background_gradient(cmap="Greens", axis=0)

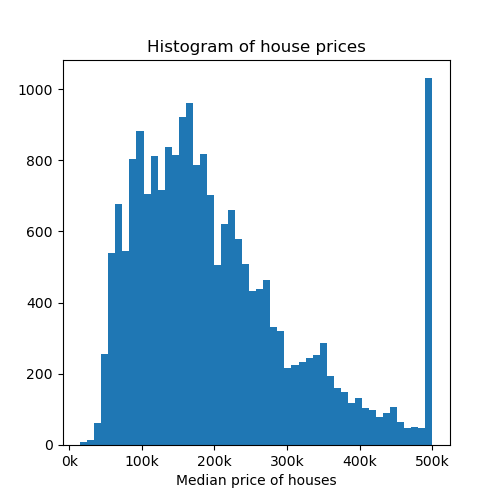

Now let’s visualize a histogram of the price of the houses.

fig, axs = plt.subplots(1, 1, figsize=(5, 5))

axs.hist(y, bins=50)

axs.set_xlabel("Median price of houses")

axs.set_title("Histogram of house prices")

axs.xaxis.set_major_formatter(FormatStrFormatter("%.0f" + "k"))

plt.show()

Let’s now create the different splits for the dataset, with a training, conformalize and test set. Remember that the conformalize set is used to conformalize the prediction intervals.

X_train_conformalize, X_test, y_train_conformalize, y_test = train_test_split(

X, y["MedHouseVal"], random_state=RANDOM_STATE

)

2. Optimizing estimator

Before estimating uncertainties, let’s start by optimizing the base model in order to reduce our prediction error. We will use the LGBMRegressor in the quantile setting. The optimization is performed using RandomizedSearchCV to find the optimal model to predict the house prices.

estimator = LGBMRegressor(

objective="quantile", alpha=0.5, random_state=RANDOM_STATE, verbose=-1

)

params_distributions = dict(

num_leaves=randint(low=10, high=50),

max_depth=randint(low=3, high=20),

n_estimators=randint(low=50, high=100),

learning_rate=uniform(),

)

optim_model = RandomizedSearchCV(

estimator,

param_distributions=params_distributions,

n_jobs=-1,

n_iter=10,

cv=KFold(n_splits=5, shuffle=True),

random_state=RANDOM_STATE,

)

optim_model.fit(X_train_conformalize, y_train_conformalize)

estimator = optim_model.best_estimator_

3. Comparison of MAPIE methods

We will now proceed to compare the different methods available in MAPIE used for uncertainty quantification on regression settings. For this tutorial we will compare the “cv”, “Jackknife plus after Bootstrap”, “cv plus” and “conformalized quantile regression”. Please have a look at the theoretical description of the documentation for more details on these methods.

We also create two functions, one to sort the dataset in increasing values of y_test and a plotting function, so that we can plot all predictions and prediction intervals for different conformal methods.

def sort_y_values(y_test, y_pred, y_pis):

"""

Sorting the dataset in order to make plots using the fill_between function.

"""

indices = np.argsort(y_test)

y_test_sorted = np.array(y_test)[indices]

y_pred_sorted = y_pred[indices]

y_lower_bound = y_pis[:, 0, 0][indices]

y_upper_bound = y_pis[:, 1, 0][indices]

return y_test_sorted, y_pred_sorted, y_lower_bound, y_upper_bound

def plot_prediction_intervals(

title,

axs,

y_test_sorted,

y_pred_sorted,

lower_bound,

upper_bound,

coverage,

width,

num_plots_idx,

):

"""

Plot of the prediction intervals for each different conformal

method.

"""

axs.yaxis.set_major_formatter(FormatStrFormatter("%.0f" + "k"))

axs.xaxis.set_major_formatter(FormatStrFormatter("%.0f" + "k"))

lower_bound_ = np.take(lower_bound, num_plots_idx)

y_pred_sorted_ = np.take(y_pred_sorted, num_plots_idx)

y_test_sorted_ = np.take(y_test_sorted, num_plots_idx)

error = y_pred_sorted_ - lower_bound_

warning1 = y_test_sorted_ > y_pred_sorted_ + error

warning2 = y_test_sorted_ < y_pred_sorted_ - error

warnings = warning1 + warning2

axs.errorbar(

y_test_sorted_[~warnings],

y_pred_sorted_[~warnings],

yerr=np.abs(error[~warnings]),

capsize=5,

marker="o",

elinewidth=2,

linewidth=0,

label="Inside prediction interval",

)

axs.errorbar(

y_test_sorted_[warnings],

y_pred_sorted_[warnings],

yerr=np.abs(error[warnings]),

capsize=5,

marker="o",

elinewidth=2,

linewidth=0,

color="red",

label="Outside prediction interval",

)

axs.scatter(

y_test_sorted_[warnings],

y_test_sorted_[warnings],

marker="*",

color="green",

label="True value",

)

axs.set_xlabel("True house prices in $")

axs.set_ylabel("Prediction of house prices in $")

ab = AnnotationBbox(

TextArea(

f"Coverage: {np.round(coverage, round_to)}\n"

+ f"Interval width: {np.round(width, round_to)}"

),

xy=(np.min(y_test_sorted_) * 3, np.max(y_pred_sorted_ + error) * 0.95),

)

lims = [

np.min([axs.get_xlim(), axs.get_ylim()]), # min of both axes

np.max([axs.get_xlim(), axs.get_ylim()]), # max of both axes

]

axs.plot(lims, lims, "--", alpha=0.75, color="black", label="x=y")

axs.add_artist(ab)

axs.set_title(title, fontweight="bold")

Here, we use MAPIE to return the predictions and prediction intervals. We will use an confidence_level=CONFIDENCE_LEVEL, (this is the target coverage for our prediction intervals). Note that that we will use symmetrical residuals for the CQR.

STRATEGIES = {

"cv": {

"class": CrossConformalRegressor,

"init_params": dict(method="base", cv=10),

},

"cv_plus": {

"class": CrossConformalRegressor,

"init_params": dict(method="plus", cv=10),

},

"jackknife_plus_ab": {

"class": JackknifeAfterBootstrapRegressor,

"init_params": dict(method="plus", resampling=50),

},

"conformalized_quantile_regression": {

"class": ConformalizedQuantileRegressor,

"init_params": dict(),

},

}

CONFIDENCE_LEVEL = 0.8

y_pred, y_pis = {}, {}

y_test_sorted, y_pred_sorted, lower_bound, upper_bound = {}, {}, {}, {}

coverage, width = {}, {}

for strategy_name, strategy_params in STRATEGIES.items():

init_params = strategy_params["init_params"]

class_ = strategy_params["class"]

if strategy_name == "conformalized_quantile_regression":

X_train, X_conformalize, y_train, y_conformalize = train_test_split(

X_train_conformalize,

y_train_conformalize,

test_size=0.3,

random_state=RANDOM_STATE,

)

mapie = class_(estimator, confidence_level=CONFIDENCE_LEVEL, **init_params)

mapie.fit(X_train, y_train)

mapie.conformalize(X_conformalize, y_conformalize)

y_pred[strategy_name], y_pis[strategy_name] = mapie.predict_interval(

X_test, symmetric_correction=True

)

else:

mapie = class_(

estimator,

confidence_level=CONFIDENCE_LEVEL,

random_state=RANDOM_STATE,

**init_params,

)

mapie.fit_conformalize(X_train_conformalize, y_train_conformalize)

y_pred[strategy_name], y_pis[strategy_name] = mapie.predict_interval(X_test)

(

y_test_sorted[strategy_name],

y_pred_sorted[strategy_name],

lower_bound[strategy_name],

upper_bound[strategy_name],

) = sort_y_values(y_test, y_pred[strategy_name], y_pis[strategy_name])

coverage[strategy_name] = regression_coverage_score(y_test, y_pis[strategy_name])[0]

width[strategy_name] = regression_mean_width_score(y_pis[strategy_name])[0]

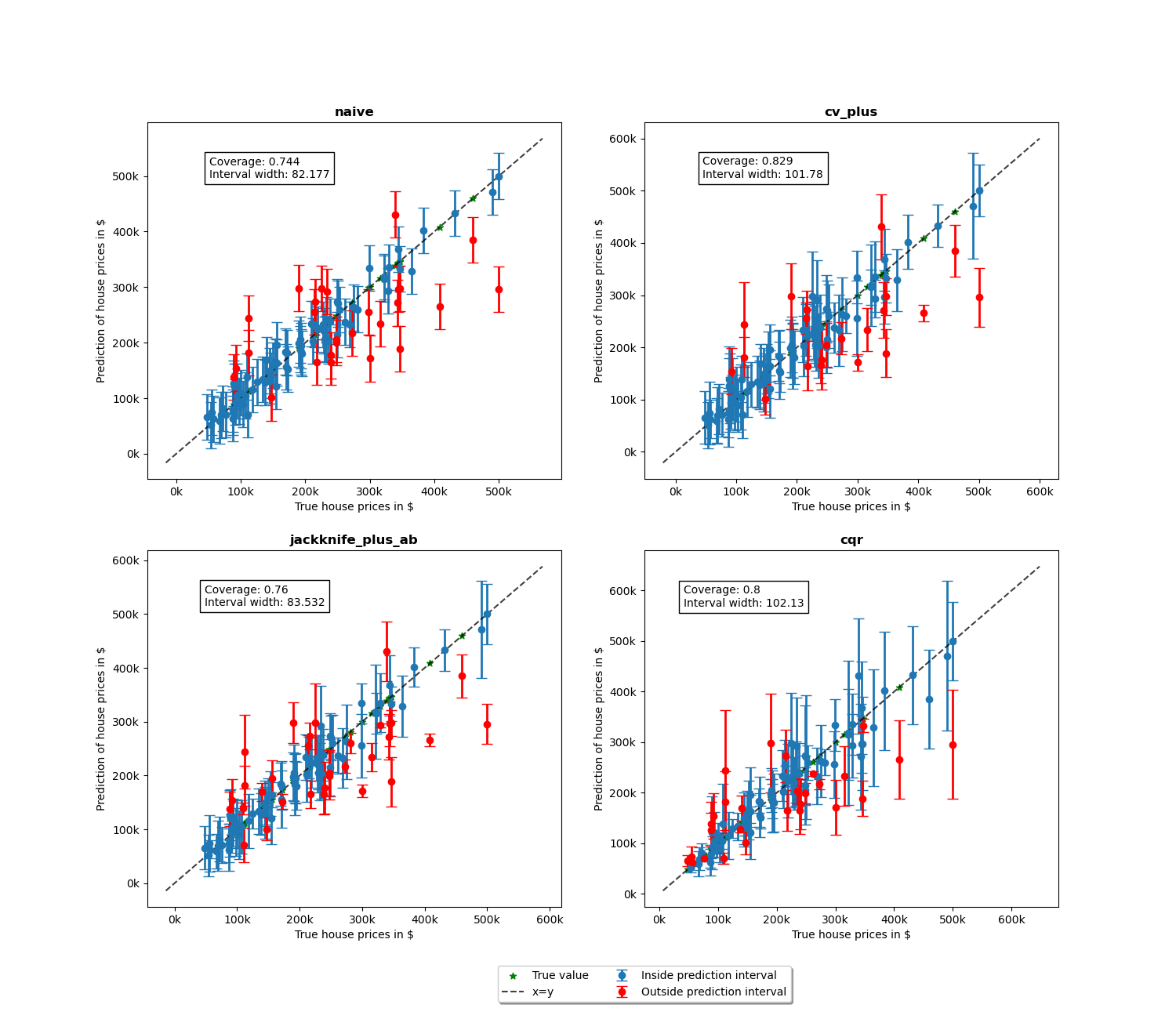

We will now proceed to the plotting stage, note that we only plot 2% of the observations in order to not crowd the plot too much.

perc_obs_plot = 0.02

num_plots = rng.choice(len(y_test), int(perc_obs_plot * len(y_test)), replace=False)

fig, axs = plt.subplots(2, 2, figsize=(15, 13))

coords = [axs[0, 0], axs[0, 1], axs[1, 0], axs[1, 1]]

for strategy_name, coord in zip(STRATEGIES.keys(), coords):

plot_prediction_intervals(

strategy_name,

coord,

y_test_sorted[strategy_name],

y_pred_sorted[strategy_name],

lower_bound[strategy_name],

upper_bound[strategy_name],

coverage[strategy_name],

width[strategy_name],

num_plots,

)

lines_labels = [ax.get_legend_handles_labels() for ax in fig.axes]

lines, labels = [sum(_, []) for _ in zip(*lines_labels)]

plt.legend(

lines[:4],

labels[:4],

loc="upper center",

bbox_to_anchor=(0, -0.15),

fancybox=True,

shadow=True,

ncol=2,

)

plt.show()

We notice more adaptability of the prediction intervals for the conformalized quantile regression while the other methods have fixed interval width.

def get_coverages_widths_by_bins(

want, y_test, y_pred, lower_bound, upper_bound, STRATEGIES, bins

):

"""

Given the results from MAPIE, this function split the data

according the the test values into bins and calculates coverage

or width per bin.

"""

cuts = []

cuts_ = pd.qcut(y_test["cv"], bins).unique()[:-1]

for item in cuts_:

cuts.append(item.left)

cuts.append(cuts_[-1].right)

cuts.append(np.max(y_test["cv"]) + 1)

recap = {}

for i in range(len(cuts) - 1):

cut1, cut2 = cuts[i], cuts[i + 1]

name = f"[{np.round(cut1, 0)}, {np.round(cut2, 0)}]"

recap[name] = []

for strategy in STRATEGIES:

indices = np.where((y_test[strategy] > cut1) * (y_test[strategy] <= cut2))

y_test_trunc = np.take(y_test[strategy], indices)

y_low_ = np.take(lower_bound[strategy], indices)

y_high_ = np.take(upper_bound[strategy], indices)

if want == "coverage":

recap[name].append(

regression_coverage_score(

y_test_trunc[0], np.stack((y_low_[0], y_high_[0]), axis=-1)

)[0]

)

elif want == "width":

recap[name].append(

regression_mean_width_score(

np.stack((y_low_[0], y_high_[0]), axis=-1)[:, :, np.newaxis]

)[0]

)

recap_df = pd.DataFrame(recap, index=STRATEGIES)

return recap_df

bins = list(np.arange(0, 1, 0.1))

binned_data = get_coverages_widths_by_bins(

"coverage", y_test_sorted, y_pred_sorted, lower_bound, upper_bound, STRATEGIES, bins

)

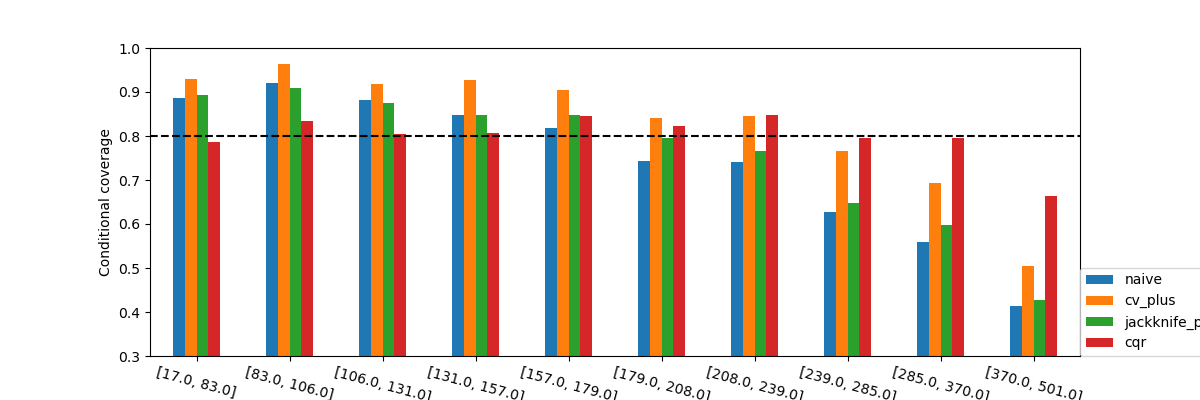

To confirm these insights, we will now observe what happens when we plot the conditional coverage and interval width on these intervals splitted by quantiles.

binned_data.T.plot.bar(figsize=(12, 4))

plt.axhline(CONFIDENCE_LEVEL, ls="--", color="k")

plt.ylabel("Conditional coverage")

plt.xlabel("Binned house prices")

plt.xticks(rotation=345)

plt.ylim(0.3, 1.0)

plt.legend(loc=[1, 0])

plt.show()

None of the methods seems to have conditional coverage at the target confidence_level. However, we can clearly notice that the CQR seems to better adapt to large prices. Its conditional coverage is closer to the target coverage not only for higher prices, but also for lower prices where the other methods have a higher coverage than needed. This will very likely have an impact on the widths of the intervals.

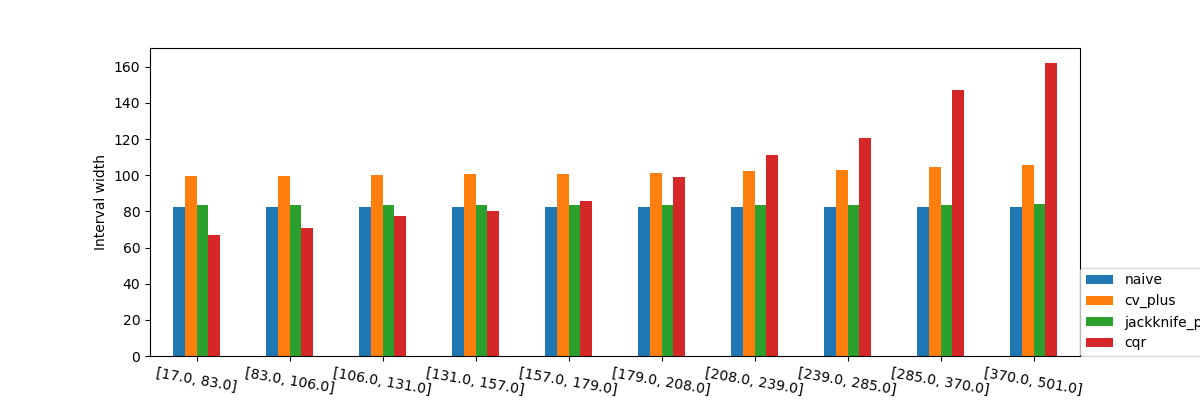

binned_data = get_coverages_widths_by_bins(

"width", y_test_sorted, y_pred_sorted, lower_bound, upper_bound, STRATEGIES, bins

)

binned_data.T.plot.bar(figsize=(12, 4))

plt.ylabel("Interval width")

plt.xlabel("Binned house prices")

plt.xticks(rotation=350)

plt.legend(loc=[1, 0])

plt.show()

When observing the values of the the interval width we again see what was observed in the previous graphs with the interval widths. It’s important to note that the prediction intervals are shorter when the estimator is more certain.

Total running time of the script: (1 minutes 26.600 seconds)